Venmo’s monetization engine looks a lot more like a diversified fintech platform.

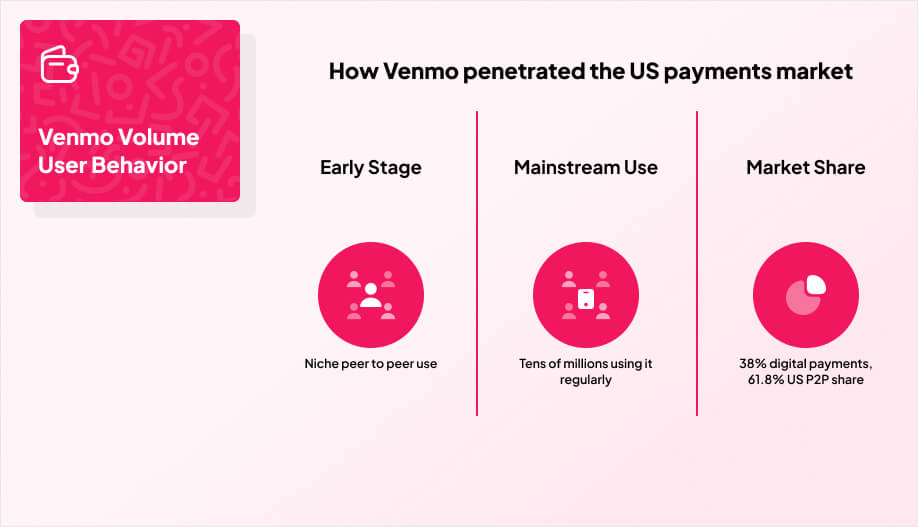

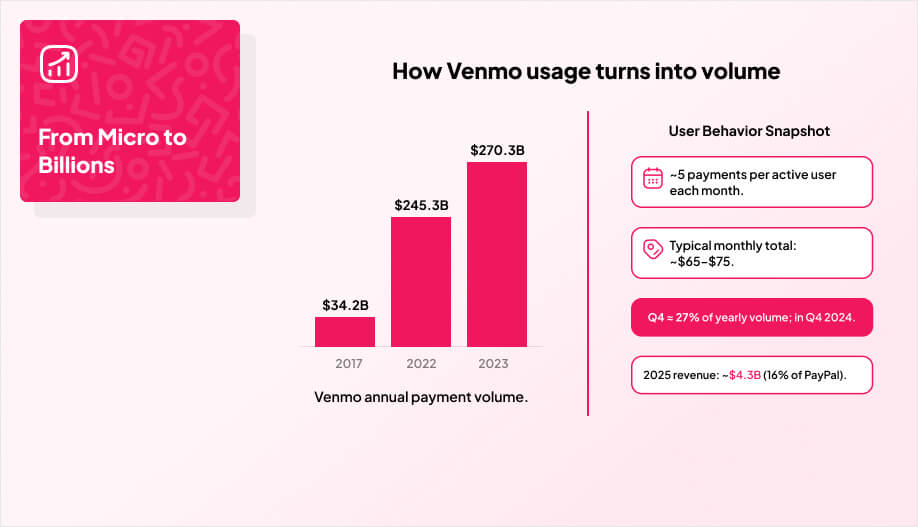

The user feed and simple payback flows keep people engaged. The business model lives in the background, where millions of small transactions and merchant checkouts turn into real fees. This growth is mirrored in Venmo’s reported Total Payment Volume statistics, which track the billions of dollars processed on the platform each quarter.

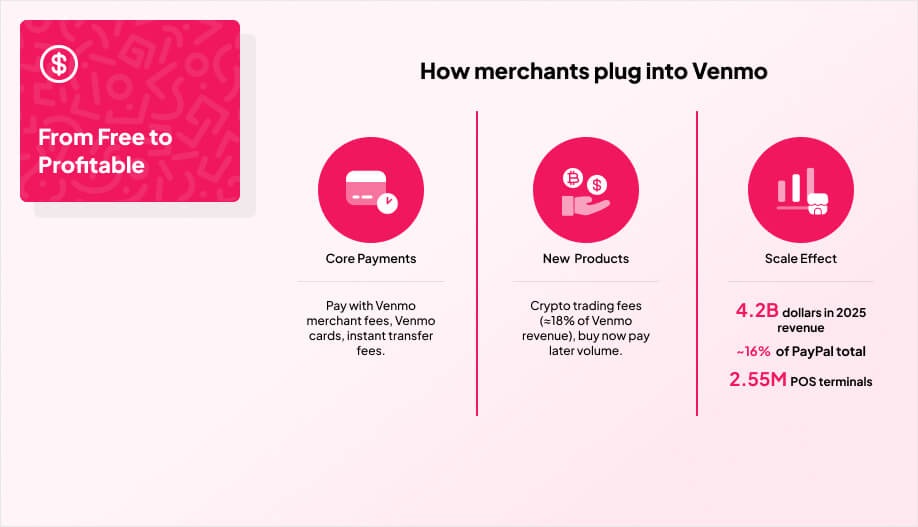

Most of the engine is still classic payments. Pay with Venmo merchant fees, interchange from the Venmo debit and credit cards, and instant transfer fees make up the bulk of revenue. In 2025, Venmo brought in roughly 4.3 billion dollars and about 16% of PayPal’s total revenue according to PayPal’s reporting, which tells you how much cash you can pull from a “no subscription” consumer app once the volume is there.

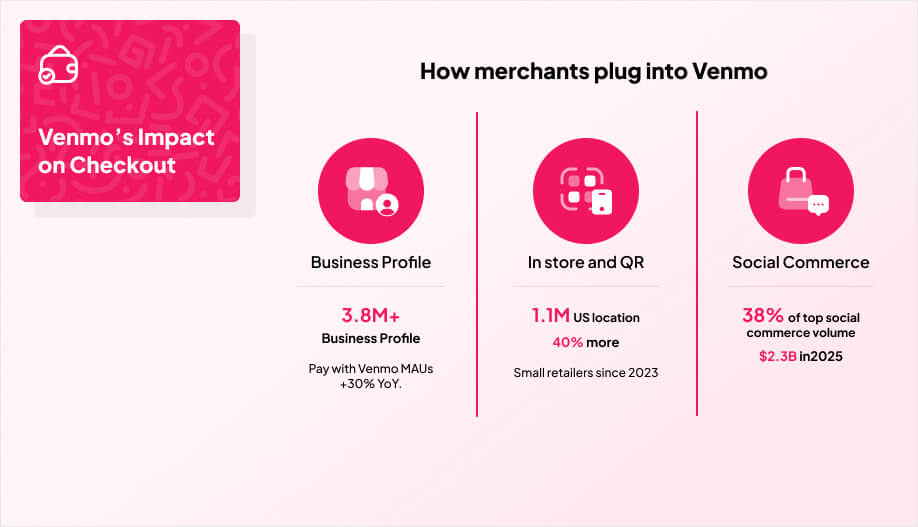

Merchant service fees and in store acceptance at roughly 2.55 million terminals are a big part of that, since they monetize the same users who started with simple peer to peer transfers.

On top of that base layer, Venmo has added higher margin products. Crypto trading fees now account for an estimated 18% of Venmo revenue as users buy, sell, and hold Bitcoin and other assets inside the app. Buy now, pay later volume, including PayPal Pay Later, pushes quarterly payments revenue higher and shows how critical pay later options have become to PayPal’s growth strategy overall. None of these products feel bolted on to end users. They show up as optional tools inside an app that already handles their day to day money movement.

The takeaway is to not start by stuffing a product with monetization tricks. You start by building a payment experience that becomes a habit. Then you find the points in that flow where merchants, power users, or higher risk actions can reasonably carry fees.

If you are designing your own fintech product, Venmo’s mix of merchant fees, card usage, instant transfers, and optional add ons is a useful blueprint for how to turn high engagement into a diversified revenue stack without breaking trust.